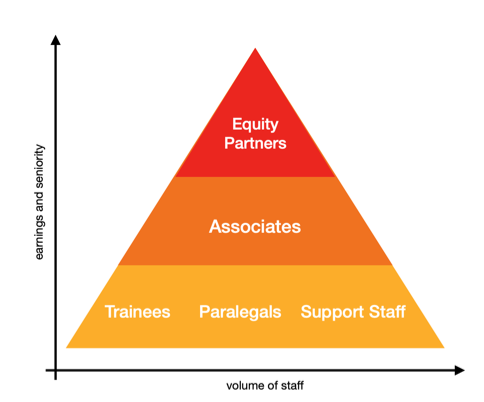

The digitisation of law is revolutionising legal practice by not only reducing workload for lawyers individually, but streamlining firms at an organisational level. As highlighted by Susskind’s The Future of the Professions, the legal field has been slow to embrace technology; law has been historically grounded in structure and tradition, which is echoed by firms’ linear partnership hierarchy [Image 1][1]. However, legal technology (LegalTech) is distorting this long-standing “pyramid” model. This article considers the consequences of LegalTech within the three main employment categories of firms (junior staff, associates, and partners), and how the pyramid model of law firms is being deconstructed.

Firms are under increasing pressure from clients to reduce legal fees, and LegalTech’s ability to process data at a faster pace than any employee makes this possible. Due diligence document-reviewing software Kira Systems — which is currently used by four of the five Magic Circle firms — claims to a time saving of 90%, and similarly, eDiscovery platform Brainspace has the capability of analysing 750,000 documents in just two hours[2]. With LegalTech automating laborious tasks that would traditionally be the reserve of paralegals and trainees, we can begin to understand how this pyramid model is changing.

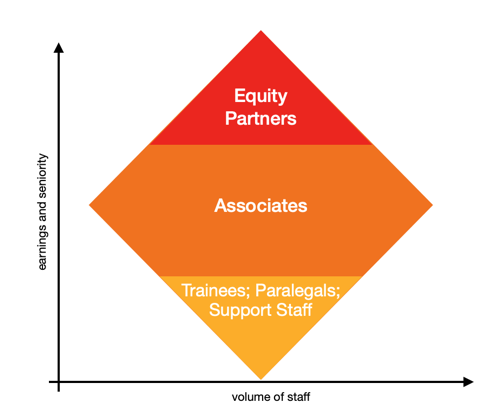

LegalTech is usually licensed on an annual basis, which, whilst expensive, is lower than the comparative salaries of a team of support staff. Therefore, the volume of staff in this bottom segment of the pyramid is continually reducing due to the increasing employment of LegalTech. In fact, Deloitte forecasts that globally, around 114,000 legal jobs are likely to be automated or eliminated in the next 20 years, with most of these being junior jobs[3]. Due to the reduction of these roles, it is likely that a diamond shaped model [Image 2] will be replacing the current pyramid model.

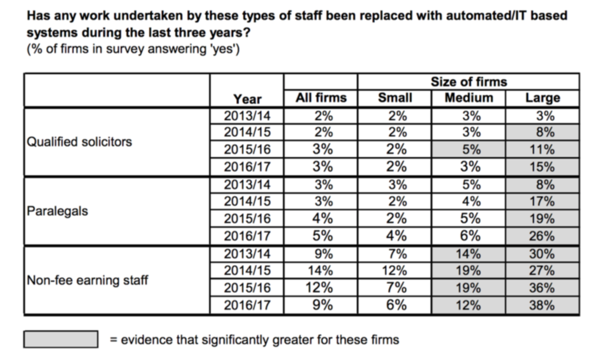

Susskind stipulates that systems could outperform 40% of the work of junior lawyers and support staff — noting that this has been acknowledged since 2011 — and the research survey in Image 3 corroborates this, highlighting that the last five years have seen the automation of up to 38% of tasks traditionally done by paralegal and non-fee earners[4].

Cutting these jobs not only reduces legal employment, but makes for an even more constricted and inaccessible legal field. For many, working as a paralegal provides a crucial stepping stone to a training contract and eventual qualification. Therefore, especially in larger firms — as evidenced by Image 3— getting one’s ‘foot in the door’ will be increasingly difficult; and whilst the Solicitors Regulation Authority (SRA) aims to encourage accessibility to legal qualification through the new Solicitors Qualifying Exam (SQE) structure, this reduction of paralegals and non-fee earners as a result of LegalTech only has the opposite effect.

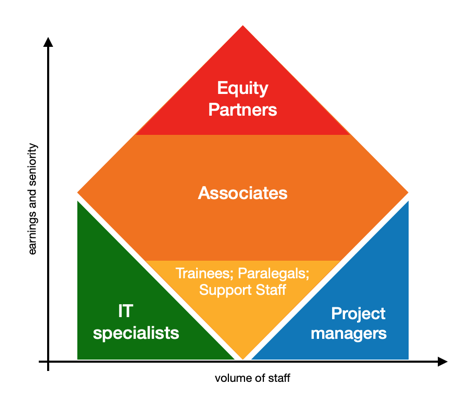

However, we can expect this reduction in headcount to be counterbalanced: as innovation of LegalTech expands, entirely new teams of IT and project management staff will be necessary. For this reason, some researchers expect the diamond shape to develop into a “rocket” shape [Image 4], with a team of fee-earners flanked by technical staff. By recruiting those from a range of practical backgrounds, this shift could arguably make the legal field more accessible than ever.

As suggested by both the diamond and rocket model, LegalTech places increasing responsibility on associates. Just as clients expect lower fees, there is now an expectation of a much faster turnaround of work, placing a pressure on all lawyers. With less opportunity to delegate to junior staff, this would be particularly felt by associates.

As put by Susskind, LegalTech is now “moving from the back office to the front office”: it is not only process-based work being automated, but more complex tasks such as drafting, which would traditionally be the reserve of associates[5]. This means that the role of associates is fundamentally changing, putting more emphasis on non-computational skills such as abstract analysis, creative problem solving, and intuition.

Time for a PEP talk?

As LegalTech becomes a necessary investment within firms, with HSBC reporting that 75% of the Top 50 UK firms plan to “significantly” invest in their Practice Management Systems by 2023, we can expect to see operational expenses rise[6]. And since Profit per Equity Partner (PEP) is affected by expenditure — especially in firms not operating on an “eat what you kill” basis — technology has the potential to fluctuate partners’ drawings.

Firms offer little transparency on how much they actually spend on licensing, or operating, LegalTech. However, by considering Allen & Overy’s Fuse incubator — a significant example of LegalTech innovation — and analysing the Firm’s Annual Reports surrounding its 2017 launch, we can speculate the weight of this expense. Following the construction of “tech innovation space” Fuse, Allen & Overy’s 2018 Annual Report evidenced a £15.9m rise in “intangible technological assets” in addition to a significant £98.8m rise in operating costs of staff and “other expenses” alone[7]. Crucially, the Firm’s partner profit pool fell by 18% in this window, making for a significant dent in PEP. Since these changes follow five years of consistent PEP and expenditure within the Firm, we can infer Allen & Overy’s Fuse as a contributor to this expense, especially given that PEP has since climbed back by 6%.

Therefore, LegalTech investment has the potential to fluctuate PEP dividends. Since the very concept of partnership entails resilience, and accepting liability for the firm’s business financially as well as legally — as evidenced by the current pandemic, where many firms have suspended partner distributions — we would certainly not expect partners to walk away following temporary reductions in PEP. However, to be cynical, arranging a sabbatical during a wave of LegalTech investment could be personally strategic for equity partners. And realistically, oscillations in partner drawings could cause tensions between General Counsel, who usually instigate innovation within firms, yet receive a fixed salary themselves.

As Fieldfisher’s strategist Katherine McPherson forecasts, we may see the very model of partnership change as a result of investment in LegalTech[8]. So, what form might this take?

PEP would be most volatile following LegalTech investment within small-to-medium sized firms, where expenditure will have a relatively greater impact on profits. In this instance, firms could consider a more consistent, “lockstep” model or an option of salaried partnership. Ultimately, LegalTech is a long-term investment for firms — improving turnover, efficiency, and identity within the legal market — and could therefore be a test of partners’ longevity and commitment to the growth of a firm, over their own PEP drawings.

The T-shaped lawyer

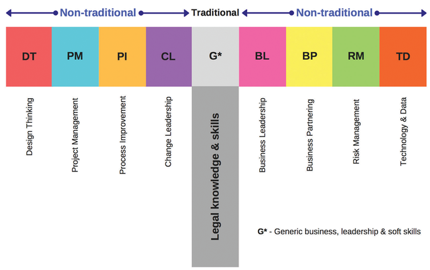

Whilst these structural changes may appear detrimental to the legal field, LegalTech has only invigorated law from a once-archaic industry to a future-facing one. As Deloitte’s leading technology partner notes, “The story [of LegalTech] is one of disruption, and only those businesses that understand and harness the new technologies will survive to tell the tale”[9]. Therefore, firms must now innovate and invest; and similarly, lawyers themselves should be resilient to these ongoing industry changes. In conclusion, as research points to the concept of the future-facing “T-shaped Lawyer” — that is, grounded in law but straddling a spectrum of other industries and skill sets [Image 5] — we can be certain that a key sector of this T is Technology.

Author: Charlotte Cocker

Edited: Panteleimon Athanasiou, Bryher Rose

Further Reading:

https://www.ft.com/content/c3a9347e-fdb4-11e5-b5f5-070dca6d0a0d

References:

[1]Richard and Daniel Susskind, The Future of the Professions, 2015.

[2]CMS LLP (CMS website, service solutions) <https://cms.law/en/gbr/online-services/smart-services/cms-by-design/case-study-saving-time-and-money-with-brainspace> last accessed, 19th June 2020.

[3]Deloitte UK, Technology in Law Firms: the case for disruptive technology in the legal profession, 2017.

[4]The Future of Justice: In conversation with Richard Susskind (interview). <https://www.youtube.com/watch?v=R0yTLqMpUuQ> last accessed, 19th June 2020.

[5]Ibid.

[6]Financing Investments in Legal Tech: peer group analysis, HSBC, 2018.

[7]Annual Report and Financial Statement, Allen & Overy, 2018 & 2019.

[8]The Future of Law Firms: An Interview with Fieldfisher (Katherine McPherson) <https://www.law.ac.uk/ultra/>

[9]Deloitte UK, Technology in Law Firms: the case for disruptive technology in the legal profession, 2017.